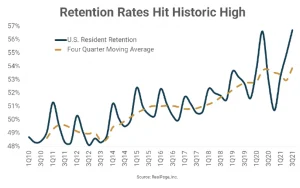

The multifamily sector’s resilience continues to attract investment from a broad range of investors. Real estate investors are remain optimistic that property values and investment volumes will accelerate in 2021. Many expect suburban and secondary markets to experience more renter and investor demand than urban assets in primary markets. .

Fannie Mae: Fannie recently announced new guidance on Streamlined Rate Locks (SRLs) for conventional and MAH loans (excluding Small, Seniors, and Student). Fannie will be approving SRL waivers for Tier three and four loans with strong repeat sponsors. On approved SRLs, Fannie is expected to remove the requirement for third party reports and may extend the requirement to close within 45 days of Rate Lock to 60 days. This should increase Fannie’s competitiveness in the index lock market.

For conventional $3 million+ and MAH loans with three plus years of IO, Fannie will consider approving modified reserves.

· Tier 2 New Guidance: 12 month IO P&I. For a loan with LTV =/< 70%: Six months of IO P&I. Strong or Priority Borrower or MHC (regardless of DTS) at any LTV: Six months of IO P&I.

· Tier 3 New Guidance: Strong or Priority Borrower or MHC: no reserves.

Freddie Mac: Freddie reduced fixed-rate conventional and TAH Cash Preservation spreads by 10 bps but increased floating rate spreads by five bps for the same business. Additionally, the credit revolver and bridge pricing grids increased by five bps.

Life Company: Pressure mounts as Life Cos ramp up volume in an effort to get back to pre-pandemic levels. Many portfolio managers have an increased need for short term paper (5-7 years) and floating rate money. Industrial and multifamily remain as the focus, though more attention will be given to the other asset classes to enhance velocity. Some firms are firmly in the low leverage/low risk camp and are willing to reduce coupons to 2.0-2.25%. Short term in lease-up multifamily loans is becoming popular with lenders meeting their desire for yield and short duration.

FHA: HUD still has a large pipeline and has issued commitments in multifamily for over $12 billion in loans over the first four months. HUD is focused on its implementation of the new MAP Guide as we head into the new HUD administration (to be officially confirmed). HUD continues to have a large pipeline and has issued commitments in multifamily for over $12 billion in loans over the first four months.

CMBS: Volume low as spreads on new originations come in. Most recently, The debt market has been very favorable to conduit transactions. Spreads on AAAs from the first two conduit deals of 2021 were almost 10 bps tighter than the last deal issued in 2020. Spreads are now in the low 200 bps for leverage up to 70%. Additionally, if leverage in less than 70%, interest only for the full term is available.